The Marketplace Exit Strategy: How to Reclaim Your Customers (and Your Margins)

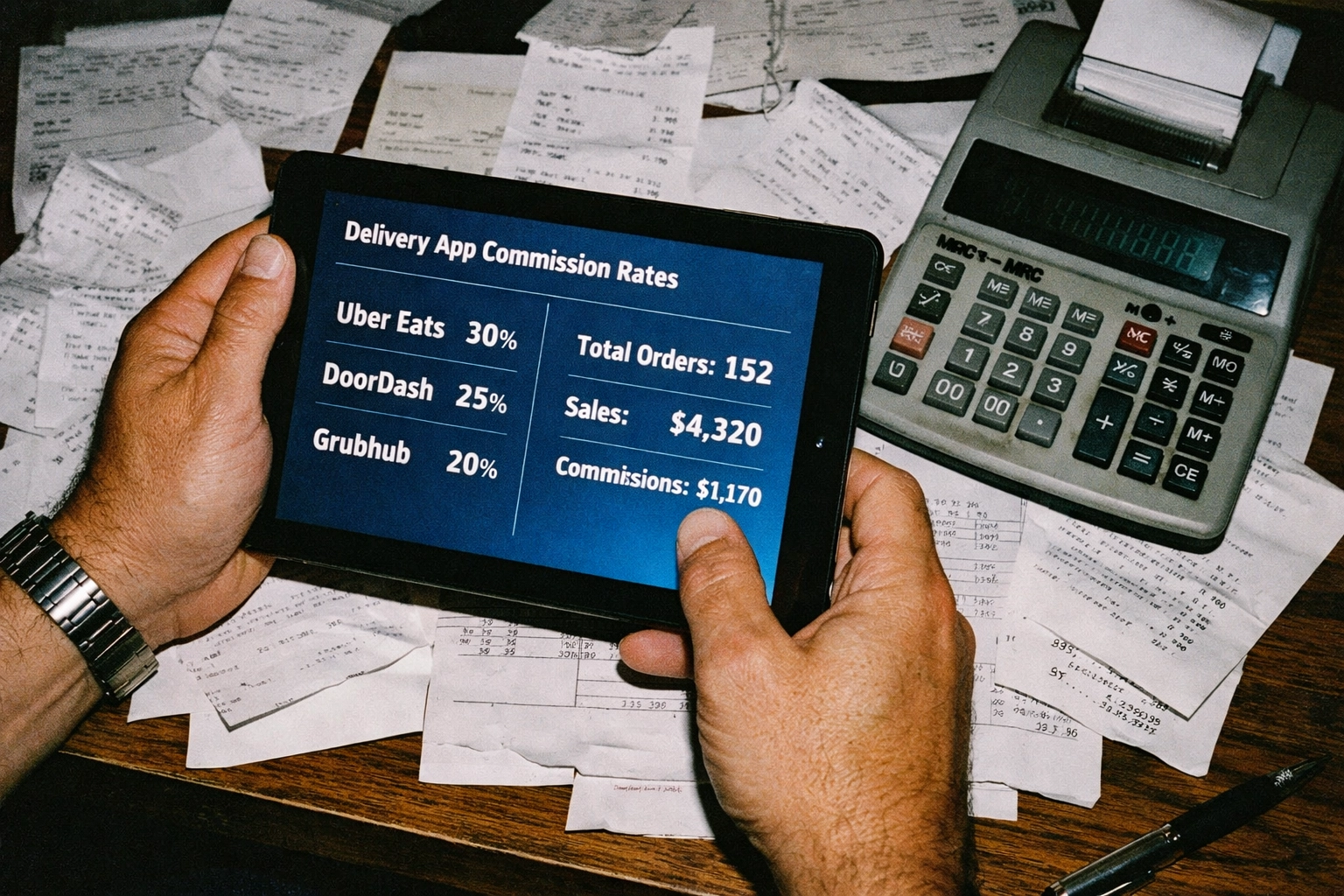

Here's the uncomfortable truth: every Deliveroo or Uber Eats order that comes through your kitchen is costing you 30% in commission. For a five-site group doing £2 million in delivery annually, that's £600,000 handed over to a marketplace that owns the customer data, controls the pricing, and treats your brand like a line item.

The maths is brutal. But the long-term cost is worse.

Because you're not just losing margin. You're losing customer ownership. Every guest who orders via a marketplace is recorded in their database, not yours. When they come back, it's to the app, not to your brand. You're renting access to your own customers.

The good news? There's a clear exit path. Mid-market and enterprise restaurant groups are quietly moving away from marketplace dependency, reclaiming their guests, and rebuilding their margin structure. It's not about going cold turkey on Deliveroo overnight. It's about building your own direct channel, incentivising the shift, and using technology to make your owned platform better than the marketplace experience.

Here's how to do it.

The Real Cost of Marketplace Dependency

Let's start with what you're actually paying for.

Commission rates are the obvious hit:

- Deliveroo: 30–35%

- Uber Eats: 30–35%

- Just Eat: 14% (plus delivery fees if using their couriers)

But the hidden costs stack up fast:

- Lost customer data: You can't build loyalty when you don't know who ordered.

- No pricing control: Marketplaces dictate discounting, bundling, and promotional mechanics.

- Brand dilution: Your restaurant sits in a feed of 50 competitors, judged purely on speed and price.

- Zero repeat behaviour insight: You can't personalise, upsell, or nurture guests you don't recognise.

For a 10-site group doing £4 million in annual delivery, that 30% commission is £1.2 million. But the inability to convert those guests into direct customers? That's the compounding cost that gets worse every year.

The Three-Part Exit Framework

Moving away from marketplaces isn't about flipping a switch. It's about building a parallel infrastructure that's better, faster, and more profitable. Here's the playbook.

1. Build Your Own Direct Channel (And Make It Frictionless)

Guests won't leave Deliveroo for a clunky checkout or a slow mobile site. Your direct platform has to be as good, or better, than the marketplace experience.

This means:

- Branded ordering that feels like your restaurant, not generic white-label tech.

- Mobile-first design with Apple Pay and Google Pay for one-tap checkout.

- Integrated loyalty that rewards direct orders, not marketplace ones.

The key differentiator? Recognition. Marketplaces treat every order like it's the first. A proper Guest Experience Engine remembers preferences, past orders, and behaviour across every channel, dine-in, delivery, and collection. That's the unlock.

Storekit's Single Guest Identity Layer does exactly this. It sits above your POS and unifies every touchpoint. When a guest orders delivery on Tuesday and dines in on Friday, you know it's the same person. That means smarter upsells, personalised recommendations, and the ability to say "the usual?" even on a delivery order.

2. Switch to Direct Delivery (Without Building Your Own Fleet)

The second blocker is logistics. Most restaurant groups don't want to manage their own couriers. Fair enough.

The solution? Uber Direct.

It's Uber's white-label courier service. You get the same drivers and reliability as Uber Eats, but the order comes through your platform. The guest never sees Uber Eats. You own the transaction, the data, and the relationship.

How Uber Direct fees actually work (in plain English)

Uber Direct is typically pay-per-delivery, not a percentage commission. The delivery cost is usually based on factors like:

- Distance

- Vehicle type (bike/scooter/car/van, where available)

- Local market conditions / time of day (availability)

So while the merchant is billed a flat fee per delivery, you also choose what delivery fee the customer pays at checkout.

That means your effective delivery cost to you is usually:

- Effective delivery cost = Uber Direct delivery fee you’re billed − delivery fee you charge the customer

This is exactly how e-commerce brands think about shipping with carriers like UPS or DPD: delivery is a utility cost you either pass through, subsidise, or mark up slightly. It’s not “a percentage of the meal” in the way marketplace commission is.

So what’s the commercial difference vs Uber Eats?

- Uber Eats takes 30–35% of the order value (plus you still don’t own the customer)

- Uber Direct is a known cost per drop, and you can control how much of it you recover via your customer-facing delivery fee

A simple way to think about the economics:

- If an Uber Direct drop costs you £6 and you charge the guest £4 delivery, your effective cost is £2 (you’re subsidising delivery a bit to drive conversion).

- If the drop costs £6 and you charge £6, your effective cost is £0 (delivery is pass-through).

- If you charge £7, your effective cost is -£1 (you’re effectively funding packaging/ops with delivery margin).

Storekit integrates directly with Uber Direct, so the hand-off is seamless. Orders placed on your branded platform get routed to Uber's driver network automatically. You get the delivery infrastructure without the marketplace tax.

3. Use AI Personalisation to Increase AOV on Direct Orders

Once guests are ordering direct, the next move is to make those orders more profitable. Not through discounting, through intelligent upselling.

This is where AI personalisation becomes a commercial lever, not a buzzword.

Here's how it works:

- A guest who always adds extra toppings gets a "build your own" prompt at checkout.

- A regular who orders every Friday gets a reminder on Thursday afternoon.

- A high-AOV customer sees premium add-ons (wine, desserts, sides) that match their ordering history.

The result? 10–15% AOV uplift on direct orders, driven by relevance, not random cross-sells.

Storekit's AI engine analyses guest behaviour across every interaction, what they've ordered before, when they order, what they pair together, and surfaces personalised prompts in real time. It's not guessing. It's using actual data to replicate what a great server does: offer the right thing at the right moment.

The Commercial Reality: What This Looks Like in Practice

Let's map this to a real scenario.

Example: 8-site fast-casual group, £3.5M annual delivery revenue

Current state (marketplace-dependent):

- 80% of delivery via Uber Eats and Deliveroo

- 30% average commission

- Annual commission cost: £840,000

- Zero customer data or repeat behaviour visibility

After implementing direct channel:

- 60% of delivery shifted to direct platform (via incentives and better UX)

- 40% still on marketplaces (for discovery and reach)

- Direct orders use Uber Direct on a pay-per-delivery model

- Marketplace orders remain at 30%

New annual “effective cost” (fees, not commission):

- Direct orders (60% of £3.5M = £2.1M):

- Assume £6 average Uber Direct cost per drop and £4 delivery fee charged to the guest

- Effective cost per order = £2

- If AOV is ~£28, direct order volume ≈ £2.1M / £28 = 75,000 orders

- Direct delivery effective cost ≈ 75,000 × £2 = £150,000

- Marketplace orders (40% of £3.5M = £1.4M at 30%): £420,000

- Total: £570,000

Savings: £270,000 per year driven by shifting from percentage commission to a pay-per-delivery model (with partial fee recovery from the guest).

But here's the compounding part:

- AI personalisation increases AOV on direct orders by 12% (from £28 to £31.36).

- That's an extra £252,000 in annual revenue from the same customer base.

- Owned customer data enables retention campaigns, reducing reliance on paid ads.

Total financial impact: £294,000+ in year one.

And it scales. As more guests shift to direct, the margin improvement accelerates.

How to Execute the Transition (Without Losing Sales)

The biggest fear is that pulling back from marketplaces will tank order volume. It won't, if you do it strategically.

Phase 1: Build the direct channel (Months 1–2)

- Set up your branded ordering platform with mobile-first UX.

- Integrate Uber Direct for courier logistics.

- Ensure your POS is connected so orders flow seamlessly into the kitchen.

Phase 2: Incentivise the shift (Months 3–4)

- Offer 10% off first direct order (via email, SMS, or in-store QR codes).

- Launch a loyalty programme that only works on direct orders.

- Add free delivery thresholds that beat marketplace pricing.

Phase 3: Drive awareness (Months 4–6)

- Use in-store signage and receipts to promote direct ordering.

- Retarget marketplace customers via email (if you've captured their data in-store).

- Run limited-time "direct-only" menu items or early access offers.

Phase 4: Optimise and scale (Months 6+)

- Use AI personalisation to increase AOV on repeat direct orders.

- Gradually reduce marketplace promotional spend.

- Monitor the shift ratio and adjust incentives as needed.

The goal isn't to eliminate marketplaces overnight. It's to own the customer relationship and shift the economics in your favour.

Why the Guest Identity Layer Is the Foundation

None of this works without unified guest data.

If a customer orders via your app, dines in, and then collects a takeaway, those should connect to one profile. Most restaurant tech treats each channel as a silo. That's why CRMs are full of duplicates and your "loyal" guests aren't being recognised.

Storekit's Guest Identity Layer solves this by sitting above your POS and stitching every interaction together. One guest, one profile, across every channel. That's how you enable:

- Cross-channel loyalty (reward delivery orders with dine-in perks).

- Accurate lifetime value tracking.

- Intelligent AI personalisation based on real behaviour, not guesswork.

It's the infrastructure that makes the exit strategy actually executable. You can read more about how customer data unification works here.

FAQ

How long does it take to shift 50% of delivery orders to a direct channel?

Most groups see meaningful traction within 4–6 months if they're actively promoting the direct platform via loyalty incentives and in-store marketing. The speed depends on how aggressive your shift strategy is and whether you're offering clear reasons (lower prices, exclusive items, faster service) for guests to move.

Do I need to stop using Deliveroo and Uber Eats entirely?

No. Marketplaces still serve a role for customer acquisition and visibility. The goal is to reduce dependency, not eliminate them. A healthy mix is 60–70% direct, 30–40% marketplaces, enough to maintain discoverability without bleeding margin.

What's the ROI on switching to Uber Direct vs staying on Uber Eats?

For a group doing £2 million in annual delivery, switching from Uber Eats (30%) to Uber Direct (18%) saves roughly £240,000 per year in commission. That's before factoring in the AOV uplift from AI personalisation or the long-term value of owned customer data.

Can AI personalisation actually increase AOV, or is it just hype?

When it's based on real guest behaviour, not random product recommendations, yes. Groups using Storekit's AI engine see 10–15% AOV uplift on direct orders because the system learns what individual guests actually want and surfaces relevant add-ons at checkout. It's the digital version of a server who knows your order.

What if my POS doesn't integrate with direct delivery platforms?

Storekit integrates with most major POS systems (Square, Clover, and others) and sits above the POS layer, meaning it can route orders regardless of your back-end setup. If you're on a legacy system, it's worth auditing whether your POS is holding back your ability to own the guest experience. You can explore integration options here.

The Bottom Line

The marketplace exit strategy isn't about burning bridges. It's about rebalancing power.

Deliveroo and Uber Eats will always have a place for discovery and reach. But relying on them for the majority of your delivery revenue means you're paying a 30% tax on every order and renting access to your own customers.

The alternative is clear: build a direct channel, switch to cost-effective logistics via Uber Direct, and use AI personalisation to make your owned platform more profitable than any marketplace could ever be.

The groups that move first will own the customer relationship. The ones that wait will keep paying the toll.

We don't just make the world's best online ordering system